Imagine you’re building a high-speed train—one that needs to get passengers (or in this case, financial transactions) from point A to point B in record time, with absolute precision, and without a single glitch. Now, would you let that train run at full speed without rigorous safety checks? Not. The same logic applies to financial technology (FinTech) applications, where even a minor bug can result in security breaches, compliance failures, or financial losses running into millions.

According to Grand View Research, the fintech industry is booming and projected to grow at a CAGR of 17.5% from 2023 to 2030. However, as financial institutions race to roll out new applications, the pressure to maintain security, compliance, and functionality is at an all-time high. That’s where FinTech application testing comes in—a critical process that ensures these platforms work seamlessly, protect user data, and comply with financial regulations.

Unlike regular apps, FinTech applications handle sensitive data, integrate with multiple banking systems, and must comply with regulatory standards like PCI DSS, GDPR, and SOX. A single failure can mean not just financial losses but also legal consequences. For instance, in 2020, the UK’s Financial Conduct Authority (FCA) fined Commerzbank AG (London Branch) £37.8 million for failing to have proper financial crime prevention systems in place, source.

So, how does FinTech application testing work? What does it cost? How long does it take? This blog will break down the process, providing a clear roadmap for businesses navigating the complex world of FinTech testing. Whether you're a startup launching a digital wallet or a bank rolling out a new mobile app, understanding this process can save you from expensive pitfalls.

FinTech application testing is the process of ensuring that financial technology software works correctly, securely, and in compliance with regulations. It involves testing various aspects like transaction accuracy, security, performance, and system integration to prevent failures that could lead to financial loss or data breaches.

Think of it like checking a vending machine that dispenses cash instead of snacks. If it miscalculates, gives out the wrong amount, or malfunctions, people lose trust, and businesses lose money. The same goes for banking apps, digital wallets, and payment platforms—one small glitch can lead to major financial chaos.

Testing isn’t just about pressing buttons and hoping for the best. It includes stress tests to see how well an app handles a surge in transactions, security tests to guard against cyberattacks, and compliance checks to ensure it meets financial regulations like PCI DSS and GDPR.

Without proper FinTech testing, users might see incorrect balances, failed transactions, or even security breaches—just like in 2021 when a UK bank’s glitch led to thousands of customers being charged twice for transactions. That’s why rigorous testing isn’t optional—it’s a necessity.

Imagine sending money to a friend, but instead of $50, the app deducts $500. Or worse, you log in and see someone else’s account details. Sounds like a nightmare, right? That’s exactly why FinTech application testing is critical—it ensures that financial apps handle money and data securely, accurately, and reliably.

Here’s why it matters:

In short, FinTech application testing isn’t just about fixing bugs—it’s about ensuring trust, security, and reliability in a sector where even a small error can have massive consequences.

Here’s the refined version of Common Challenges in FinTech Application Testing, with all external sources clearly mentioned in brackets so you can hyperlink them as needed:

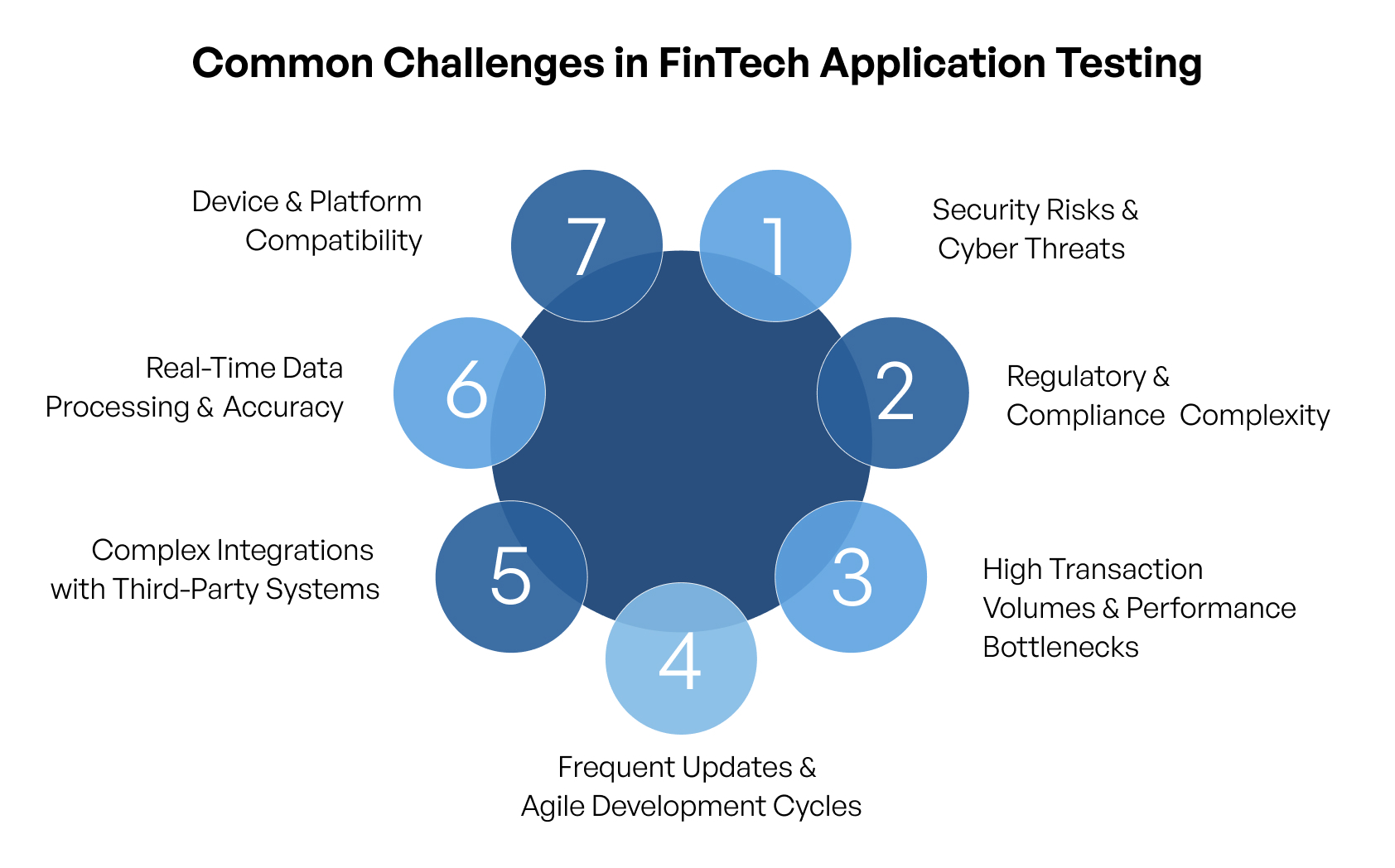

Testing FinTech applications presents unique challenges due to the sensitive nature of financial data, stringent regulatory requirements, and the need for seamless integration with various financial systems. Even minor issues can lead to significant financial losses, legal penalties, or reputational harm. Key challenges include:

FinTech applications are prime targets for cybercriminals. Comprehensive security testing is essential to identify and mitigate potential threats such as data breaches, fraud, and unauthorized access. Notably, global cybercrime costs are projected to reach $10.5 trillion annually by 2025.

FinTech applications must adhere to a myriad of regulations, including PCI DSS for payment security, GDPR for data protection, and SOX for financial reporting. Non-compliance can result in substantial fines and reputational damage. For instance, the UK's Financial Conduct Authority fined Commerzbank AG £37.8 million for inadequate anti-money laundering controls between 2012 and 2017.

FinTech applications must efficiently handle high transaction volumes, especially during peak periods like salary disbursements or market fluctuations. Performance testing ensures that applications can manage such loads without degradation, ensuring real-time processing and scalability. For example, Visa’s payment system processes around 65,000 transactions per second, highlighting the importance of load and stress testing in financial applications.

FinTech applications often integrate with various external systems, including:

Financial transactions require absolute accuracy—even a minor bug can lead to incorrect fund transfers or duplicate charges. Testers must validate:

Users access FinTech applications from various devices—smartphones, tablets, desktops, and even smartwatches. Testing ensures:

With rapid changes in regulations and user demands, FinTech apps require continuous updates. Challenges include:

FinTech applications operate in a highly regulated environment, with laws and standards governing data privacy, financial transactions, and security. Testing plays a crucial role in ensuring compliance with these regulations, helping businesses avoid hefty fines and legal consequences.

Here’s how testing ensures adherence to financial regulations:

To ensure that a FinTech application is secure, reliable, and compliant with industry standards, testing must focus on the following critical areas:

FinTech applications handle sensitive financial transactions, integrate with banking systems, and must comply with strict regulations. A structured testing process is crucial to ensuring security, compliance, and seamless functionality. Below is a detailed breakdown of the FinTech application testing process from planning to post-deployment monitoring.

Before testing begins, the business and regulatory requirements must be clearly defined. FinTech applications are subject to industry regulations such as GDPR, PCI DSS, SOX, and AML, making compliance a critical focus.

This phase defines the testing scope, methodologies, and automation strategies to ensure efficiency and thorough validation.

A well-configured test environment ensures that the system behaves as expected under real-world conditions.

This step ensures that the core functionalities of the FinTech application work as intended, covering user interactions and financial transactions.

Security testing identifies vulnerabilities that could lead to fraud, data breaches, or unauthorized access.

FinTech applications must handle large transaction volumes and peak load scenarios without failures.

Also Read: : Importance of Application Performance Testing in the Cloud

FinTech applications must adhere to strict financial and data protection regulations.

FinTech applications rely heavily on third-party APIs for payments, banking operations, and fraud prevention.

Users access FinTech applications across multiple platforms, requiring thorough cross-platform testing.

Before deployment, real users must validate the application’s usability and overall experience.

Even after deployment, ongoing testing ensures the application remains secure, stable, and compliant.

Also Read: The Role of Continuous Testing in DevOps

The duration of FinTech application testing depends on multiple factors, including the complexity of the application, regulatory requirements, and the scope of testing. On average, a comprehensive testing process can take anywhere from 8 weeks to 6 months.

Factors that can extend testing timelines include:

The cost of FinTech application testing depends on the size, complexity, and regulatory needs of the application. Testing costs typically range from $50,000 to $500,000+, depending on various factors:

The cost of FinTech application testing is influenced by several factors, including the complexity of the application, security requirements, compliance needs, and testing methodologies. Here are the key elements that impact the overall cost:

Also Read: Security Compliance Management

Also Read: The Role of Security Testing for LLMs Implementations in Enterprises

Infgraphic: 10 mistakes to Avoid in Performance Testing

Testing a FinTech application is a complex but essential process to ensure security, compliance, performance, and reliability. Given the sensitive nature of financial data and real-time transactions, even a small bug can result in significant financial losses or legal consequences.

A well-planned testing strategy helps identify vulnerabilities, prevent fraud, and enhance user trust while ensuring the application meets regulatory standards. The cost and duration of testing depend on factors such as application complexity, security needs, third-party integrations, compliance requirements, and performance demands.

Advanced technologies are transforming fintech software testing by enabling automation, real-time risk assessment, and AI-driven analytics for enhanced security. Generative AI further accelerates testing by autonomously generating test cases, predicting edge cases, and optimizing QA workflows.

Good question! Financial regulations like PCI DSS, GDPR, SOX, and AML are complex and constantly evolving, so staying compliant requires more than just checking boxes. We follow a structured process to cover all the bases: First, we map your app’s functionalities against relevant financial regulations. Then, we perform data privacy tests to ensure customer information is encrypted and stored securely. We also validate KYC (Know Your Customer) and AML (Anti-Money Laundering) checks to prevent fraudulent activity. Finally, we conduct audit log tests to confirm that all financial transactions are properly recorded and traceable in case of an investigation. Compliance isn’t just about passing a test—it’s about building trust with your users and regulators.

Good question! Financial regulations like PCI DSS, GDPR, SOX, and AML are complex and constantly evolving, so staying compliant requires more than just checking boxes. We follow a structured process to cover all the bases: First, we map your app’s functionalities against relevant financial regulations. Then, we perform data privacy tests to ensure customer information is encrypted and stored securely. We also validate KYC (Know Your Customer) and AML (Anti-Money Laundering) checks to prevent fraudulent activity. Finally, we conduct audit log tests to confirm that all financial transactions are properly recorded and traceable in case of an investigation. Compliance isn’t just about passing a test—it’s about building trust with your users and regulators.

Good question! Financial regulations like PCI DSS, GDPR, SOX, and AML are complex and constantly evolving, so staying compliant requires more than just checking boxes. We follow a structured process to cover all the bases: First, we map your app’s functionalities against relevant financial regulations. Then, we perform data privacy tests to ensure customer information is encrypted and stored securely. We also validate KYC (Know Your Customer) and AML (Anti-Money Laundering) checks to prevent fraudulent activity. Finally, we conduct audit log tests to confirm that all financial transactions are properly recorded and traceable in case of an investigation. Compliance isn’t just about passing a test—it’s about building trust with your users and regulators.

Good question! Financial regulations like PCI DSS, GDPR, SOX, and AML are complex and constantly evolving, so staying compliant requires more than just checking boxes. We follow a structured process to cover all the bases: First, we map your app’s functionalities against relevant financial regulations. Then, we perform data privacy tests to ensure customer information is encrypted and stored securely. We also validate KYC (Know Your Customer) and AML (Anti-Money Laundering) checks to prevent fraudulent activity. Finally, we conduct audit log tests to confirm that all financial transactions are properly recorded and traceable in case of an investigation. Compliance isn’t just about passing a test—it’s about building trust with your users and regulators.

Good question! Financial regulations like PCI DSS, GDPR, SOX, and AML are complex and constantly evolving, so staying compliant requires more than just checking boxes. We follow a structured process to cover all the bases: First, we map your app’s functionalities against relevant financial regulations. Then, we perform data privacy tests to ensure customer information is encrypted and stored securely. We also validate KYC (Know Your Customer) and AML (Anti-Money Laundering) checks to prevent fraudulent activity. Finally, we conduct audit log tests to confirm that all financial transactions are properly recorded and traceable in case of an investigation. Compliance isn’t just about passing a test—it’s about building trust with your users and regulators.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)